Top Countries Where You Should Not Invest in Real Estate why here is the reason From my own work with clients, I’ve seen many people rush into buying property because they think only about popular destinations and beautiful headlines, without taking a close look at the local market. This is a serious oversight because markets differ by country and even by city, and not all behave the same. Some areas become overheated and prone to sharp price corrections, so even attractive prices today can hide properties that remain illiquid for years. In this environment, the traditional approach that feels good and guaranteed for growth often turns unreliable.

In several major cities, the square meter cost has drifted away from real purchasing power, which hurts returns for investors expecting lower risk than regular bank deposits. If you’re not prepared to review the worst cases of buying real estate, you miss how this concept—by nature—is complex, and how this article was created from three independent rankings that highlights bad locations and specific types of risk an investor may face.

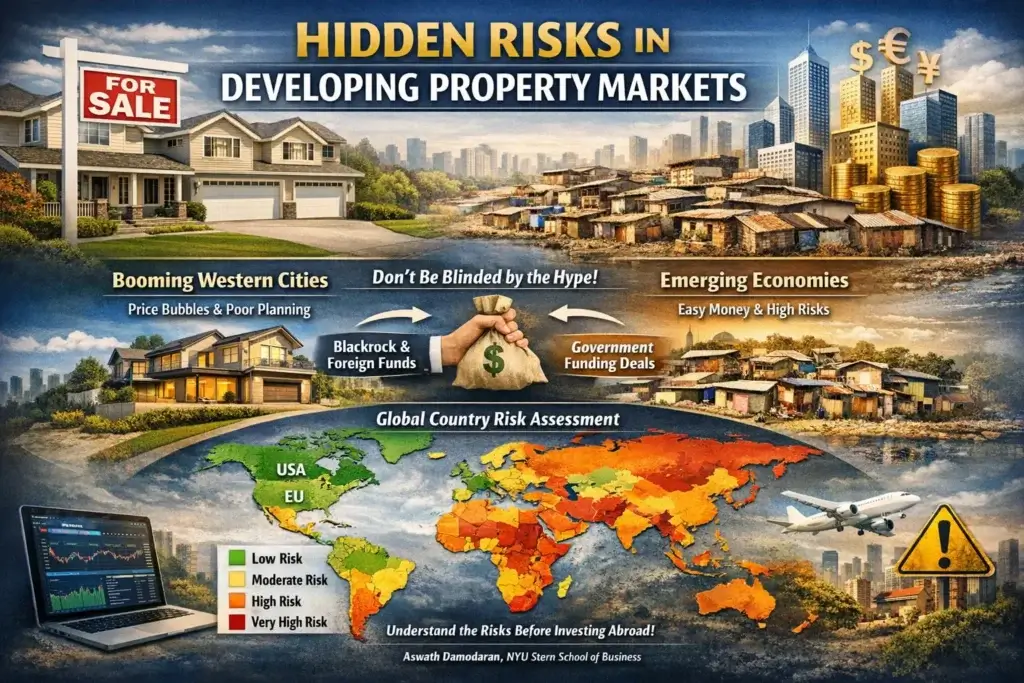

Many concerns my clients have brought involve challenges of investment overseas, where usually a native individual calls it home and you might not notice issues like you would in the United States. Being respectful, obviously, and building trust help me look to deliver information they know is sympathetic and clear, correcting misconceptions and ideas that apply to investing completely different ballgames. You may benefit from content originally posted on Advisor Channel—sign up to a free mailing list—with visualizations, financial markets insights for advisors and clients, showing risk from another angle: rapid growth in emerging economies brings opportunities but also raises the question of exposure abroad, as analyzed in a graphic that shows each country around the world, based on analysis by Aswath Damodaran, New York University, Stern School Business.

Table of Contents

Hidden Risks in Developing Property Markets

Probably everyone is aware that house prices have gone insane in western countries like Canada, USA, West Europe, New Zealand, Sydney, and Melbourne, where a multi millionaire still faces serious real estate investment risks. From my experience in buying, I’ve seen poor planning lead people to believe they are quickly becoming rich, but instead they should study why a selected country that looks peaceful, open, and free may still be a weak market. Many focus on getting loans and financial packages, assuming only the richer choose houses in big cities as safer places to put in money, while ignoring suburban areas once bought for dirt cheap with hope they evolve into a city later.

In poor countries, I noticed investors try to understand what Blackrocks are doing, buying real estate with getting packages from the US, Japan, and EU, sometimes practically free money from governments that finance deals. I often explain to clients why this plan can go wrong, as originally posted on Advisor Channel—you can sign up to a free mailing list with beautiful visualizations of financial markets that help advisors and clients see risk in investing in another country. With given rapid growth in emerging economies, opportunities present themselves, but this raises the question of exposure abroad, analyzed in a graphic that shows country risk around the world, based on analysis by Aswath Damodaran, New York University, Stern School Business.

Major Factors That Impact the Real Estate Market

Economic Reality Behind Risky Property Markets

From my experience reviewing global deals, the strength of the overall economy significantly impacts the real estate market, because consumers lose the ability to support housing prices when conditions weaken, and this greatly depends on key factors like unemployment, income, and growth; the state plays a huge part in the amount of money available for people to buy homes, while politics, natural gas, oil, and production contribute to sudden policy shifts that turn once-stable countries into high-risk places for real estate investment.

How Interest Rates Shape Risky Property Markets

From what I’ve seen working across borders, politics, banks, and the global economy can all influence the real estate market when it comes to interest rates, and this is a key factor in how mortgage rates are established because it sets the cost for banks to borrow money. In weaker countries, I’ve watched sudden policy shifts change lending overnight, where lower interest rates typically lead to lower mortgage rate offers from banks, making risk look smaller than it really is.

The problem is that this decreases the monthly mortgage payments a home-buyer must pay for a given mortgage amount, and the smaller the monthly payment, the more affordable a loan is to potential home-buyers. I’ve seen how this fact can increase the loan amount for which home-buyers are likely to get, which might drive up property prices, especially in countries where rising debt hides deeper real estate risks.

Population Trends That Signal Property Risk

From my experience advising overseas buyers, knowledge of demographic factors such as age, race, gender, and median income of a particular area will help you expect future market trends and better position your homes for sale, because knowing whether an area is home to an aging population or is attractive to young families can better prepare you to show the neighborhood to the appropriate buyer, and in many countries with shrinking or mismatched populations, this imbalance quietly increases the risk of long-term real estate investment.

Why Location Can Make or Break Your Investment

From years of reviewing overseas deals, I’ve heard the phrase location, location, location on and on, but what exactly does it mean in risky markets; location is not just something that translates into price, it reflects some key factors that impact your life and lifestyle, such as quality of local schools, proximity to local employment opportunities, and proximity to social environment and shopping centers, and in weaker countries these basics are often missing, even in cities that look attractive on paper. I’ve seen how these three preferences, proximity to school, work, and entertainment shopping, form a trio that makes an immensely valuable property, and when one element fails, the entire real estate investment becomes far more fragile.

Before investing in real estate, it’s important to closely watch key factors such as employment trends, population growth, home value appreciation, affordability, and local safety. When these indicators are weak, even well-known cities can become risky investment choices. Based on these factors, the following locations stand out as some of the worst places to invest in real estate.

Pueblo, Colorado

Pueblo struggles with weak economic momentum and safety concerns, which limit long-term property growth and rental demand.

- Unemployment rate: 20%

- Job growth: 0.85%

- Population growth: 0.65%

- Increase in home values: 6.2%

- Years to pay off a single-family home: 6.56

- Crime rate: 75.54 per 1,000 residents

Honolulu, Hawaii

Despite its global appeal, Honolulu’s high property costs and slow value growth make returns challenging for most investors.

- Employment growth: 2.2%

- Population growth: 0.65%

- Increase in home values: 1.3%

- Years to pay off a single-family home: 36.29

Anchorage, Alaska

Anchorage faces declining population and slow employment growth, making it difficult for real estate investors to rely on appreciation or consistent demand.

- Employment growth: 0.50%

- Population growth: -0.55%

- Increase in home values: 2.3%

- Years to pay off a single-family home: 13.81

Top 5 Cities Showing Clear Signs of Overheating

From my experience reviewing global property data before moving money into major cities themselves, it is important to clarify two key indicators used to determine an overheated market: price to income and price to rent, which are universal metrics applied by banks, international research institutes to assess whether housing prices align with real economic conditions.

The price to income housing affordability ratio reflects median property values relative to household annual income, and although called a ratio, it practice shows how many years needed to purchase a home—for example, 3–5× means three to five incomes, 7–9× means seven to nine, and 10–15× means ten to fifteen, where price exceeds annual income by a factor of ten or fifteen and signals local demand can no longer sustain the market, so further growth relies on speculative external demand, a classic indicator of overheating.

The price to rent payback period shows how many years rent would be required to cover the purchase price, where 10–15 years is normal in developed economies, 15–20 years indicates overvaluation, and when the payback period exceeds twenty to twenty-five years, rental yields fall below alternative investment options, leaving the buyer essentially paying for the expectation of future price growth rather than current cash flow.

Hong Kong

HongKongremains a global benchmark for an overheatedmarket, where housingaffordabilityratiostays in the fourteentoseventeenrange, a level that internationalrankingsclassify as severelyunaffordable. Even after a pricecorrection of roughlytwenty-fivepercent from the 2022 peak, the averagepricepersquaremeterstillexceeds18to23 thousand, and the paybackperiod, when compared to comparablereturn from a bankdeposit, involvessignificantlyhigherrisk, making it a cautionary choice for investors looking for stable real estate growth.

Sydney: Real Estate Out of Reach

By 2025, Sydney reached the top position globally for housing unaffordability, with median property price rose fourteen to fifteen times annual household income. The average home price across the metropolitan area is approaching seven hundred eighty thousand dollars, which effectively moves beyond the reach of the middle class. Rental yields remain low, 2.5 to 3 percent for houses and slightly above 3 percent for apartments, as demand is driven not by economic fundamentals but catch-up market mindset and expectations of continuous growth. Any tightening in lending conditions or slowdown in migration would put pressure on prices, making Sydney a risky real estate market for new investors.

Toronto: A Market Sensitive to Risk

Over the past decade, Toronto shifted from a stable market to a high-risk one, with affordability ratio now around nine to eleven and price to rent metric in central districts exceeds twenty-four years. The average home price in the metropolitan area is about seven hundred ninety thousand dollars, while rental yields usually do not rise above 4 percent and tend to stay near 3 to 3.5 percent. Although the market has already undergone noticeable correction with rate hikes, prices remain fundamentally overvalued, and the high share of investor-driven purchases makes the market highly sensitive to changes in financial conditions, warning investors to proceed with caution.

Munich: Extremely Costly Market

Munich is considered one of the most expensive real estate markets in Europe, with average home price equals twelve to thirteen annual household incomes and price per square meter consistently remains in the eight and a half to nine thousand euro range. Rental yields are low, rarely exceed 3 percent, and under these parameters, the payback period approaches thirty to thirty-three years, which effectively removes a segment or category of viable investments, making Munich a high-risk choice for real estate investors.

Miami

The average home price in Miami is lower than other cities on this list, about five hundred seventy to six hundred thousand dollars, and considering a 3 percent price decline in 2024–2025, does not look alarming; even so, the market remains clearly overvalued, with estimated payback period of fifteen to sixteen years, above national average. The most critical issue is the rapid rise in insurance costs in coastal zones, increasing at double-digit rates despite drop in overall number of claims, which points to Miami market becoming one of the most vulnerable in North America for real estate investors.

Cities with Weak Rental Returns

The average home price in Miami is lower than other cities on this list, at about five hundred seventy to six hundred thousand dollars, and considering a 3 percent price decline during 2024–2025, it does not look alarming; even so, the market remains clearly overvalued, with an estimated payback period of fifteen to sixteen years, well above the national average. From my experience reviewing rental-heavy cities, the most critical issue is the rapid rise in insurance costs across coastal zones, increasing at double-digit rates despite a drop in the overall number of claims, which point to the Miami market having become one of the most vulnerable in North America when rental yields are taken into account.

| Paris | Paris is one of the clearest examples of a city where the price per square meter has moved far beyond what the rental market can support. In central districts, the average gross yield ranges from 2.5% to 3%, while the net yield sometimes fails to reach even 2%, making returns comparable to a standard bank deposit. |

| London | London attracts large amounts of global capital, but for investors relying on rental income, the city offers little advantage. In popular districts, yields rarely exceed 2.8% to 3.3%, while central areas often fall to 2%–2.5%, combined with very high ownership costs. |

| Singapore | Singapore shows some of the lowest rental yields in Asia, even after periods of rising demand. The average yield across many residential categories stays between 2.5% and 3.5%, and in this highly urbanized market, maintenance, repairs, and management fees reduce net income even further. |

| Shanghai | Shanghai is among the weakest performers in Asia, with rental yields consistently low at around 2% to 3%. Strict government policies, high property prices, limited access for foreign buyers, and regulated rental rates make the market better suited for residence rather than investment. |

| Tokyo | Tokyo combines relatively affordable rents for residents with high purchase costs for foreign investors. The average yield on residential properties stays near 3% to 4%, while aging buildings increase maintenance expenses, reducing overall net yield. |

Top 5 Cities in the World with the Lowest Real Estate Liquidity

From my experience reviewing failed overseas deals, low liquidity is often underestimated, yet buying property in such markets is a serious mistake, because low rental yields indicate weak cash flow while an overheated market suggests rising risk of price decline. Low liquidity means it becomes difficult to sell an asset, as a property can remain on the market for months or even years until a real buyer appears, often only after a significant price reduction, turning what looked like a safe investment into a long-term capital lock.

Cairo: A Market That Takes Time to Exit

From my experience studying emerging markets, Cairo, the capital of Egypt and the largest metropolis in North Africa, shows a deep gap between supply and the population’s purchasing power, which is enormous in scale. As a result, the average listing period in new districts often exceeds six to twelve months, and transactions usually close at prices fifteen to twenty percent below initial asking levels, while fragmentation of the market makes the situation worse, with many development projects launched without guaranteed demand.

Antalya: Supply Running Ahead of Demand

In my review of emerging coastal markets, Antalya has experienced explosive construction growth in recent years, moving far ahead of real demand, and when periods for residence permits became restricted, property buyers saw weakened foreign interest. This shift led to listing periods stretching five to eight months or longer, and against a backdrop of a volatile national currency and extremely high inflation, negotiations have become tough, with discounts of ten to fifteen percent now common, making liquidity and exit timing a serious concern for real estate investors.

Dubai: When Fast Growth Hits Liquidity

Dubai frequently appears in the news as a fast-growing city with many new projects and large-scale construction, but this gradually reduces liquidity in the secondary market. In complexes with high volume of new supply and high resale properties, units move slowly, often requiring a significant discount in certain segments. Listing periods can reach one hundred twenty to one hundred fifty days, especially in areas where dozens of buildings are released at the same time, making it difficult for investors to exit quickly.

Athens: Liquidity Challenges for Investors

In Athens, although housing once saw strong demand as buyers allowed under Greece’s golden visa rules, the tightened regulations have decreased demand, and the market has faced a sharp drop in liquidity. Listing periods in secondary housing districts often exceed one hundred sixty to one hundred eighty days, while in areas heavily oriented toward foreign buyers, the figure approaches one year, making it a challenging market for investors to sell quickly.

Johannesburg: A Market Hard to Exit

Johannesburg is one of the least liquid major markets in Africa, with only small enclaves showing stable demand. Most of the market suffers from low purchasing power and high crime levels, and listings often receive no serious interest for more than a year, even when sellers offer discounts of twenty percent or more, making it very difficult for investors to sell quickly.

To Sum Up: What Makes a Market Risky

When evaluating a city as a poor choice for buying real estate, it is not defined by a single market condition but reflects at least three different types of risk. An overheated market is shown by high price to income or price to rent ratios and a likelihood of price correction, which increases after shock events, higher interest rates, or slower economic growth. Low rental yields signal weak cash flow, which directly affect how long it take a property to pay itself before an investor can start earning real profit. This is closely linked to liquidity: illiquid properties often sit on the market and generate losses during vacancies. In practical terms, such locations should not be dismissed entirely, as they remain suitable for very wealthy buyers who intentionally lock up capital for a long period or for those solving personal need living in a specific city regardless of cost. For everyone else, the combination of overheating, weak rental performance, and poor liquidity makes these cities some of the worst choices for property investment, especially if the goal is profit.

Leave a Reply